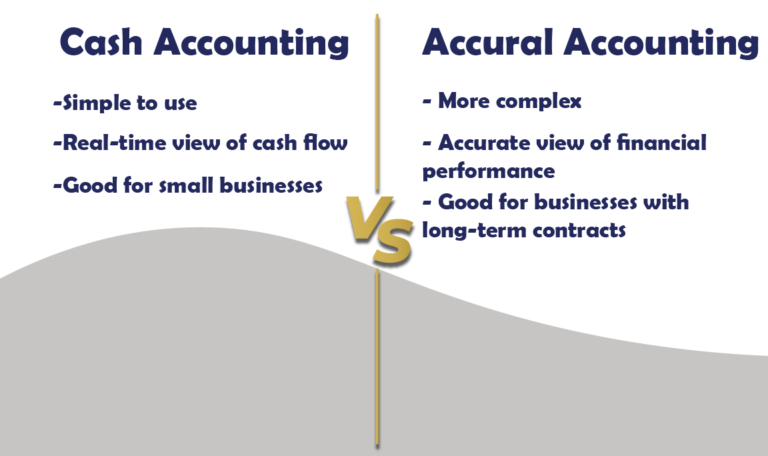

Basically, cash accounting is a pretty straightforward method. Transactions are recorded only when money is actually exchanged. In other words, when you receive money, you record it as income. And when you pay money, you record it as expenses. It is a good method for companies that are just starting out because they reflect real-time cash flow.

However, in its simplicity, it can be misleading when doing profit assessments. You see, cash accounting doesn’t show accounts receivable/payable. So if your company is bigger or has a lot of inventory, it might not be your best option.